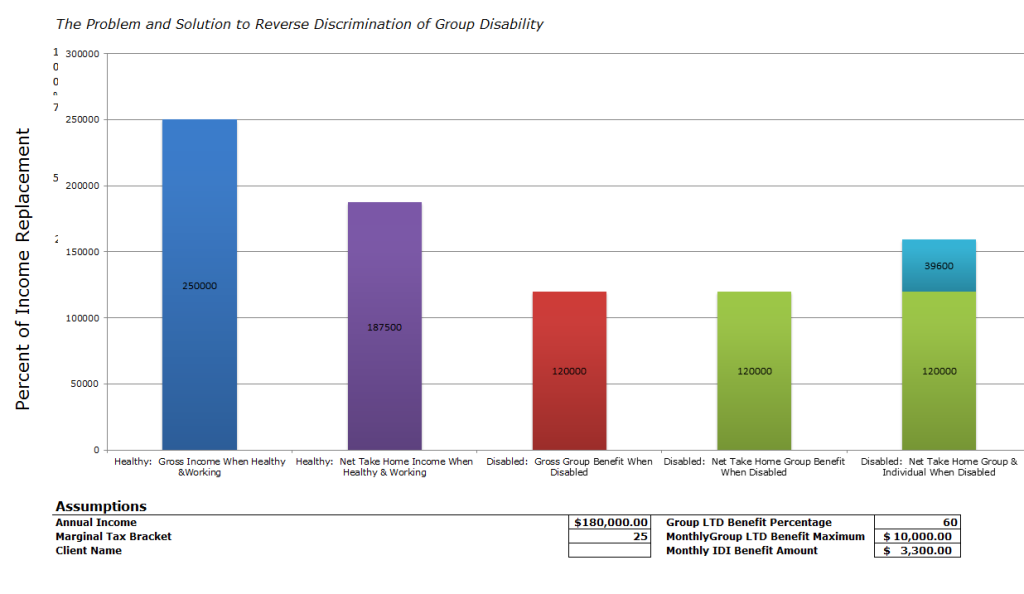

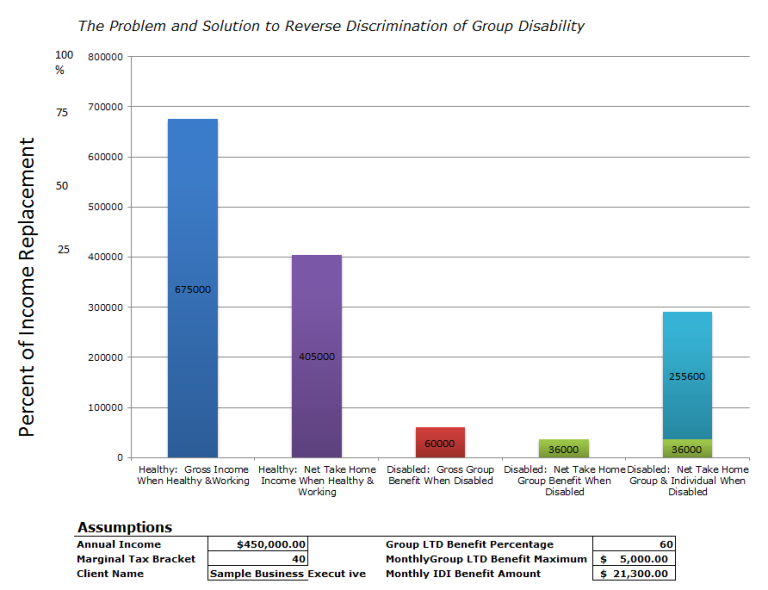

Adding the cost of your Disability Insurance to your W-2

Having disability insurance is one of the most important insurance policies you can have during your working years. If you have it through your employer, and your employer pays for it, it’s a beautiful thing. The important thing to remember here is that if your employer pays for the insurance premium, when you collect the benefit it will be taxable. Most Disability policies pay anywhere from fifty percent to seventy percent of your pre-tax income. If the employer is paying the bill for your benefits, it will be a taxable benefit. If you are only receiving fifty to seventy percent of your income and it is taxed on an after-tax basis you will only end up with thirty to forty percent of your gross income; that is not enough for you to live on. The process of having the employer add the cost of disability insurance to your W-2 is commonly neglected but very, very important.

What you need to do is approach your employer, the human resources person, or the benefits department and ask to have the cost of your disability insurance, pro-rated for just your cost out of the group, added to your W-2. Some employers will simply add the number to your existing W-2, others will issue a separate W-2 specifically for the cost of disability insurance. What this move will do is essentially make sure you pay tax on the premium although you are not paying the premium. For example, if the employer pays $1,200.00 a year for your disability premium on a pro-rated share out of the group, you will pay tax on that premium. If your tax bracket is 33% you will pay $400.00 dollars in income tax on that benefit, so the cost to you per year for this move would be $400.00 dollars. If you are young and healthy the cost is typically very low, perhaps as little as a few dollars a week. If you are older, unhealthy and/or female, the cost can be very high, may even go to a few hundred dollars each month. This is a very suboptimal scenario where you are paying tax on the premium not the benefit.

Once this is done properly, when you go to collect your disability, the benefits will be received by you income tax-free. So if your benefit only provides you with fifty to seventy percent of your income, and is not taxed, that will give you the same number of dollars at an after-tax basis that you had before. Now your income is well protected on an after-tax basis.